What if I told you that two people could earn the exact same amount of money over their lifetime, but one of them pays 30% less in taxes simply by changing when they claimed and how they pulled that income? Interested? If so, read on!

What is Tax Bracket Arbitrage?

We know what tax brackets are from our earlier post on Marginal vs Effective Tax Rates. So let’s start with a definition of “arbitrage”. Dictionary.com defines arbitrage as follows:

arbitrage NOUN

Finance. The purchase of currencies, securities, or commodities in one market for immediate resale in others in order to profit from unequal prices.

For “Tax Bracket Arbitrage”, instead of “currencies, securities, or commodities”, we’re talking about taxable income and instead of “markets”, we’re talking about tax brackets. So we can write our definition as:

tax bracket arbitrage

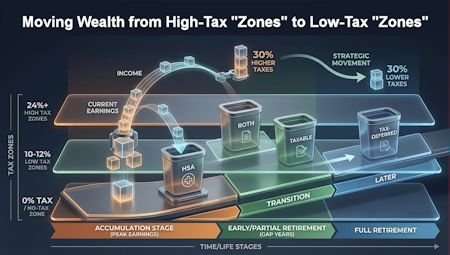

The strategic use of different account types, income classifications, and timing to move money from high-tax “zones” to low-tax (or no-tax) “zones”.

That sounds great except that you can’t just directly choose a lower tax bracket. You can, however, strategically use the various tax breaks, savings vehicles, and varying income levels at different stages of life to shift income to more preferential tax brackets. This can result in HUGE tax savings with minimal effort. In the most simplistic form, we’re manipulating when and how we take our income so that it’s in the lowest possible tax bracket when taxes become due.

IMPORTANT: We’re focusing on U.S. tax brackets and laws here. Many countries work similarly, but anything non-U.S. is outside the scope of this discussion.

Our Toolbox – The Four Buckets

The main tools at our disposal for tax bracket arbitrage are the four types of investment account types:

- Tax-Deferred

- Roth

- Taxable

- Health Savings Account (HSA)

See our previous blog post on The Four Buckets for a detailed discussion of each.

NOTE: Make sure any account type you utilize allows you to choose how you invest the money deposited (as opposed to simple interest-bearing or other poor investment vehicles). This is generally true nowadays, but check your specific accounts to be sure. The last thing you want is your money NOT to grow, or worse, lose value to inflation.

Why This Matters Now (2026 Context)

Since we are in 2026 and the One Big Beautiful Bill Act (OBBBA) has made the 2017 Tax Cuts and Jobs Act (TCJA) brackets permanent, we have a stable playing field to plan these strategies for decades to come.

Life Stages

In the FI/FIRE community, the strategies involved generally fall into 3 different stages of the FI journey:

- Accumulation: your earlier, high-earning years.

- Early/Partial Retirement: low- or no-earning years prior to age 59.5

- Full Retirement: low- or no- earning years after age 59.5

We’ll cover tax bracket arbitrage strategies for each of these in the next three blog posts of this series!