Reducing Taxes as a Wealth-Building Lever

There are three basic levers we can pull to build wealth: earn more, spend less, and reduce taxes. The first two are easily understood, although not necessarily easy to do. The third, however, is a little more difficult to understand, but still relatively easy to do.

Reducing taxes is one of the best ways to speed up your FI journey and all it takes is learning some relatively simple concepts. These concepts then allow you to employ a number of tax-saving strategies, the most common of which is tax-bracket arbitrage.

For those earlier in their FI journey, tax-bracket arbitrage usually consists of deferring taxes while in a higher tax bracket (your high earning years), until later when you’re in a lower tax bracket (like retirement). For those later in their FI journey, tax bracket arbitrage may mean withdrawing from different accounts or doing Roth conversions to avoid higher tax brackets. For this discussion, we’ll focus on the former.

Before we can understand tax bracket arbitrage, however, we need to understand what tax brackets are, how they work, and what is meant by “marginal” vs “effective” tax rates.

NOTES: Individual state taxes are beyond the scope of this discussion. You will, however, want to factor your state’s income taxes into any tax optimization strategy. FICA taxes are also beyond the scope of this discussion. However, know that FICA taxes are taken out of your pre-tax income and do not change your taxable income.

U.S. Tax Brackets Explained

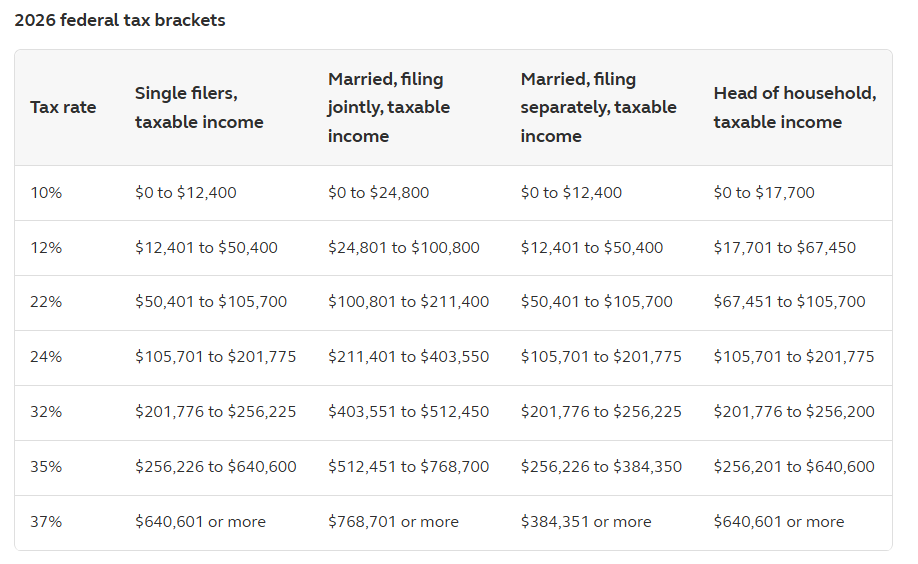

The U.S. tax system is a graduated system. In simple terms, that means the more income you have, the more taxes you pay. This is done by defining “income brackets”. The concept is simple —for each $ income range (bracket), the IRS defines the tax rate you pay. Below are the federal tax brackets for 2026.

But, before we dive into marginal vs. effective tax rates, let’s cover a couple other terms —”Filing Status” and “Standard Deduction”.

Filing Status

You can file your taxes as 1 of 4 statuses. For most, this will be either Single or Married – filing jointly.

- Single: unmarried, no dependents

- Married, filing jointly: married and filing together, combining incomes

- Married, filing separately: married but filing individual returns

- Head of household: unmarried, with one or more dependents (see IRS for full definition)

As you can see from the table above, your income tax brackets vary by filing status. “Married filing jointly” brackets are effectively double “Single” and “Married, filing separately” brackets, for example. That makes sense since two incomes are being filed on one return.

Standard Deduction

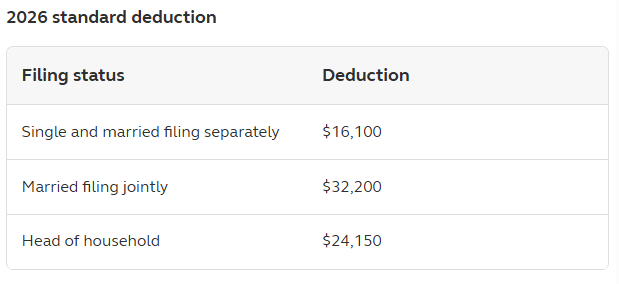

The government also allows certain “deductions” that reduce the amount of income you owe taxes on, examples include home mortgage interest and charitable contributions. Rather than require every tax payer to list these deductions, the IRS has defined a “standard deduction” that everyone gets to take. In recent years, this “standard deduction” is so generous that it’s rare to actually itemize individual deductions. For example: In 2022, 91% of tax filers took the standard deduction. The 2026 the standard deductions by filing status are shown below:

You can kind of think of the standard deduction as a 0% tax bracket. For example, Single, and married filing separately, pay no taxes on the first $16,100 of earnings. The difference is, it’s subtracted from your total earnings before to determine your taxable income and then the tax brackets above are applied. An example in the next section will clarify.

Idea: one way to think of the standard deduction is a “0% tax bracket”.

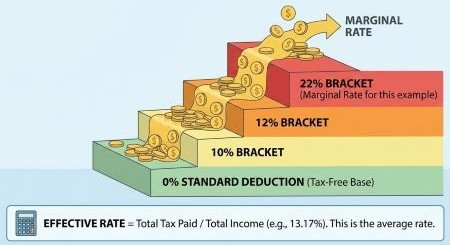

Marginal vs Effective Tax Rates

Marginal Tax Rate

Marginal tax rates are simply the tax rates listed on the left side of the “2026 federal tax brackets” table shown above. Let’s clear up a common misconception: many people think whatever tax bracket they fall in is the tax rate they pay on all their taxable income. That’s incorrect. You pay the applicable tax rate for each bracket. The taxable income that falls in each bracket is taxed at that bracket’s rate. That’s the difference between marginal and effective tax rates.

Common Misconception: The tax rate that corresponds with your total taxable income is the tax rate you pay. FALSE —each bracket is taxed at its corresponding rate.

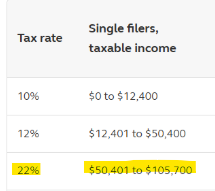

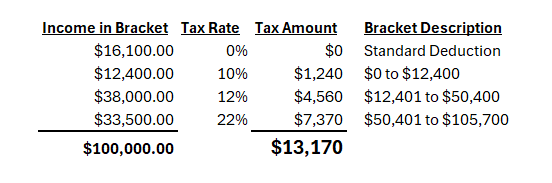

Example: Let’s say a Single filer has $100,000 gross income (that’s total income earned). After taking the standard deduction ($16,100 for single filers), they have $100,000 – $16,100 = $83,900 in taxable income. Using the table above, we see that they are in the 22% tax bracket.

But, that 22% only applies to the amount greater than $50,400. They pay 10% on the first $12,400, 12% on the portion between $12,401 and $50,400, and 22% on the amount over $50,400.

Effective Tax Rate

The above discussion sets us up perfectly to discuss your effective tax rate. The formula for effective tax rate is simply:

Effective Tax Rate = Total Tax / Total Gross Income

NOTE: some people may subtract out the standard deduction and use Taxable Income as the denominator. We’re NOT doing that here because it’s important for the full picture when doing FI tax bracket arbitrage which I’ll cover in a later post.

Total Tax

Back to our single filer earning $100,000 example, to calculate Total Tax we just need to calculate the tax paid in each bracket. We can see that our filer’s total tax burden is $13,170 after breaking her income into the tax brackets as follows:

Total Gross Income

This is simple: $100,000.

Effective Tax Rate = $13,170 / $100,000 = 13.17%

Summary

We’ve learned the difference between marginal and effective tax rates.

- Marginal Tax Rate = Tax rate of the highest applicable tax bracket (22% in our example)

- Effective Tax Rate = Tax rate calculated across entire earned income (13.17% in our example)

Why is this so important? Because it can make a huge difference doing tax bracket arbitrage for reaching FI. Again, I’ll cover this topic in a later blog post. But as a teaser, consider our single filer example here is determining whether to invest in a pre-tax account (like 401k) or a post-tax account (like Roth 401k). Since our friend’s marginal tax bracket is 22%, she could contribute up to $24,500 ($32,500 if over age 50) pre-tax in 2026. This would defer taxes at the 22% rate. Then at retirement, even if she pulls $100,000 per year from her pre-tax account, she would pay an effective tax rate of 13.17%. That’s 8.83% in tax savings. Plus, she got to earn money on that 22% of taxes the entire time up to retirement!