Welcome back! We’re continuing our four-part series on tax bracket arbitrage (TBA). In Part 1, we introduced tax bracket arbitrage and the tools available. In parts 2 through 4 we’ll cover the strategies for each of the major Life Stages: Accumulation, Early/Partial Retirement, and Full Retirement. In this post, we’re focusing on the first: Accumulation Stage.

Accumulation Stage

The Accumulation Stage of your FI journey is the first stage. It’s the early phase of life where you’re probably working full-time, earning the most money, and subsequently paying the highest taxes. The goal in this stage is to save as much as possible while still enjoying life. Each person will have their own balance of saving vs consuming that they’re comfortable with.

Why this Stage is Critical

Even though retirement may seem like a far-away dream, this is the most critical stage of your journey for retirement. These are the years that determine, by the actions you take, how well your retirement will be (or if you even retire at all). These are also the years that allow you to take full advantage of the power of compounding. See “The Time Tax / Cost of Delay” section of our previous blog post: The Urgency of Now to understand the importance of compounding.

Key Assumption

Tax bracket arbitrage (TBA) at this stage of the FI journey is based on a single important assumption.

Assumption: You will likely be in a lower tax bracket during retirement than you are now, due to these early years being your highest earning years.

While this assumption will be true for most of us, there are some things that could make that NOT true for you. Some of these include:

- Already in a low tax bracket: for whatever reason – your earnings are low, you file taxes as married but only one of you works, etc.

- U.S. raises taxes in the future: this seems unlikely since politicians who do so tend not to get re-elected. But, the U.S. is currently facing unprecedented federal debt that will have to be dealt with at some point.

- Spousal death or divorce: this would move you from married tax brackets (more favorable) to single tax brackets (less favorable). This is often referred to as “the widow’s tax”.

- Inheritance or other income: you may have inheritance, pension, or some other taxable income in retirement that keeps you in a higher tax bracket.

TBA Strategies

Your strategy will likely be a mix that’s personal to you. There’s no one-size-fits-all answer. However, there are some consistent fundamental principles to keep in mind as you design your personal strategies.

Common Strategy Principles

The following principles hold true regardless of the TBA strategy you choose:

- Save as much as reasonably possible. We’ve covered this multiple times, but it’s worth repeating; it’s the single most impactful lever you have to pull and it has a double-effect:

- It accelerates your savings. The more you save, the sooner you reach FI.

- It keeps your living expenses low. The less you learn to live on, the less you need to be FI, and the sooner you reach FI.

- Always take full advantage of your employer’s retirement plan matching. This is free money. At minimum, always contribute enough to maximize your employer’s match before directing savings anywhere else.

- Have an emergency fund. Buildup six months of living expenses in safe, post-tax accounts like high-yield savings or laddered CDs. This gives you peace of mind and options in the case of job loss or other catastrophe.

- Utilize all four buckets if possible. Having savings in each of Tax-deferred, Roth, Taxable, and HSA accounts gives you the most flexibility for life AND tax bracket arbitrage.

Strategy

The general strategy can be summarized as follows: Defer taxes on any income that’s in a higher marginal tax bracket than your effective retirement tax rate. The larger the difference between these two, the more advantageous this strategy becomes.

NOTE: Why compare our current marginal tax rate to our retirement effective tax rate? Because when we defer taxes on current earnings, we are deferring taxes in the top bracket (i.e. our marginal tax rate). This same money withdrawn at retirement will be spread across all the tax brackets (i.e. our effective tax rate).

Gathering Data

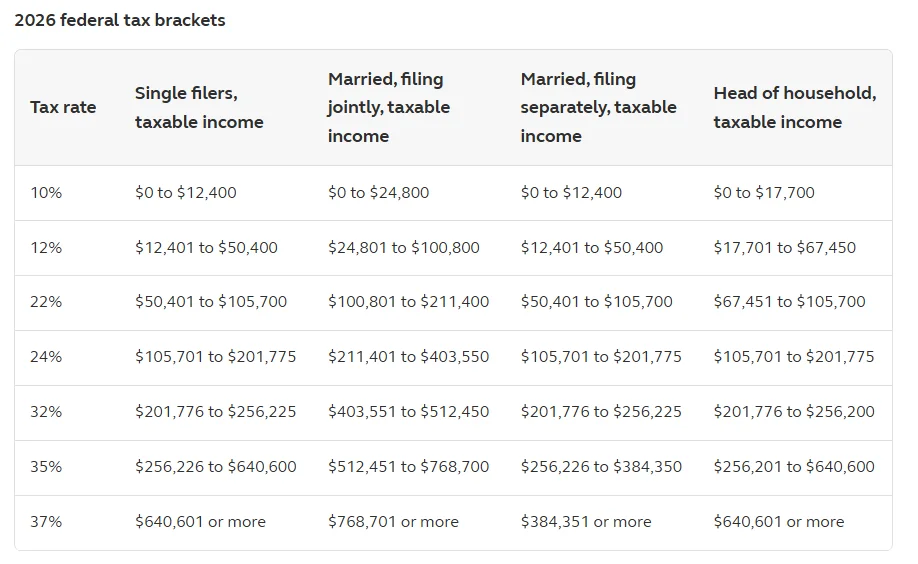

Your current marginal tax bracket is easy—use your current income and the table of federal tax brackets below. Your retirement tax bracket is tougher to determine. To estimate that, you’ll need the following data:

- Your annual retirement lifestyle expenses. This will likely change as life and priorities change; just do your best estimate given what you currently know and plan. It represents how much you’ll be pulling from your retirement accounts.

- The U.S. tax brackets at retirement. We don’t know the future; I suggest you use the current tax brackets for simplicity.

- How much of your retirement savings will be tax-deferred. This is a bit of a chicken-and-egg situation. How much you tax-defer depends on your expected retirement tax bracket and your retirement tax bracket will depend on how much you tax defer.

- Effective tax rate calculation. See our post on Marginal vs Effective Tax Rates for how to do this. NOTE: for simplicity, you could use your marginal retirement rate instead. That will give you a lower estimate of potential tax savings; but if it gets you to do this exercise, it’s well worth it. Personally, I’d suggest you do it both ways (with marginal and effective retirement tax rates) for a thorough understanding of these concepts.

Bucket Contribution Order

You’ll remember from Blog Post 012 that our four investment buckets are: Tax-Deferred, Roth, HSA, and Taxable. All of these have contribution limits with the exception of taxable, obviously. So, as you contribute to these to defer taxes, you may hit these limits while still having more savings to invest. Here’s the rough order to contribute for retirement as you hit the maximums:

- Tax-Deferred – 401(k), 403(b), Traditional IRA

- Roth – Roth IRA, Roth 401(k)

- HSA – Health Savings Account

- Taxable – Individual or Joint Brokerage accounts

You need not max out one bucket before contributing to another. There is no one-size-fits-all strategy here. For example, it may be wise to put some into an HSA for possible health issues even before you’ve maxed out Tax-Deferred and Roth. Alternatively, you may want to switch the order of HSA and Roth, to defer the absolute most income.

Alternate Strategy – If Your Retirement Tax Rate is NOT Lower

If you’re one of the few that will have more income in your retirement than you have now, you may want to skip some contributions to the Tax-Deferred and instead focus on Roth, HSA, and Taxable.

Alternate Bucket Contribution Order

- HSA – never taxable if used for healthcare

- Roth – although this is post-tax contributions, the gains & interest are never taxable

- Taxable – don’t underestimate the power of a taxable account. Capital gains and qualified dividends are taxable, but at the much lower “Capital Gains Tax Rate”. Further, capital gains grow tax-free until you decide to sell.

- Tax-Deferred – This is likely still a valuable bucket for you depending on your circumstances. IMPORTANT: if your employer matches contributions to this type of account, you should be contributing enough to get that full match in this bucket before contributing anywhere else.

Conclusion – Call to Action

In the accumulation stage of your FI journey, your goal is to save as much as possible. That includes using TBA to supercharge the impact of those savings. The TBA goal is: Defer taxes on any income that’s in a higher marginal tax bracket than your effective retirement tax rate.

Everyone’s situation is different and everyone has different priorities. It would be impossible to come up with a single strategy to fit everyone. The goal here is to increase your understanding so that you can design strategies that work for you. Use the information here to:

- Determine your current marginal tax rate

- Determine your retirement effective tax rate

- Use a spreadsheet or other tool to play “what if” scenarios with different contribution amounts and retirement withdrawal amounts.

- Remember:

- Tax-Deferred bucket contributions reduce your taxable income which may lower your current marginal tax rate.

- Roth bucket withdrawals are not taxable in retirement, so these accounts will lower your retirement effective (and marginal) tax rate.

One final consideration: Tax-Deferred savings generally have RMDs (Required Minimum Distributions). That means starting at some age, the government will require you to start taking taxable distributions from these accounts. This can force you into higher tax brackets in retirement. Be sure to research RMDs and consider them in your retirement planning.