Welcome back! We’re continuing our four-part series on tax bracket arbitrage (TBA). In Part 1, we introduced tax bracket arbitrage and the tools available. In Part 2 we discussed the accumulation stage of your FIRE journey. And here we’ll talk about the early/partial retirement phase.

Early/Partial Retirement Stage

For our purposes, we’ll define early/partial retirement as any time before age 59.5 that you leave full-time employment/wages. This could be full retirement or it could mean part-time work to fill your time or supplement your lifestyle. You’re tapping into your savings, rather than actively adding to them. The significance with age 59.5 is that this is when you can withdraw from tax-deferred retirement accounts without penalty (in the U.S.).

The goal in this stage is to enjoy life while minimizing present and future tax burden. Like all stages, each person will have their own unique situation, savings, investments, and spread across the 4 main buckets. This means your specific strategies will be unique to you.

TBA Strategies

At this stage of the FIRE journey, we’re likely all in unique and very different situations. So, more than ever, there’s no one-size-fits-all strategy. Also, there are multiple facets to consider. We’ll keep it simple here.

Gathering Data

Before we start, you’ll need to gather the following info:

- Annual income sources and amounts. In order to have a strategy, you absolutely must know all your income sources (wages, interest, dividends, etc.) and be able to project those amounts each year with reasonable accuracy. Do NOT include retirement savings drawdowns in this number.

- Savings balances by bucket type. Because each bucket type has its own tax rules, summarize your savings amounts by bucket type. See The Four Buckets for more information.

- Applicable U.S. income tax brackets. The simplest way is to just use google. Search “2026 US tax brackets”, for example. Don’t forget state taxes, if applicable.

- Applicable U.S. capital gains tax brackets. Long-term capital gains (gains on investments held more than 1 year) are taxed differently than short-term capital gains (gains on investments held 1 year or less). Note: qualified dividends are also taxed at long-term capital gains rates; that discussion is beyond the scope of this article.

- Applicable U.S. standard tax deduction. Again, just use google to find this. Note: If you itemize deductions (very few people do thanks to generous standard deductions), use your total itemized deductions instead.

- Annual lifestyle expenses. This may be the toughest data to get, but it’s worth it. Estimate your annual expenses by category, if possible. At minimum group into discretionary and non-discretionary.

Strategy

The process below will need to be repeated annually. Life is always changing and each year will have unique expenses, incomes, tax brackets, and so on.

Step 1 – Calculate Required Annual Drawdown

Calculate the amount you’ll need to pull from your savings. This is simply the difference between your total annual income and your annual lifestyle expenses.

Note: if your annual income sources include things that will not be used as income (example dividends that are set to reinvest), exclude those from the total annual income.

Annual Drawdown = Annual lifestyle expenses – Annual income

Step 2 – Determine Marginal Income and Capital Gains Tax Brackets

Using your annual income, applicable tax brackets, and applicable standard deduction, find your marginal tax rate(s). For more info see our post on Marginal vs Effective Tax Rates.

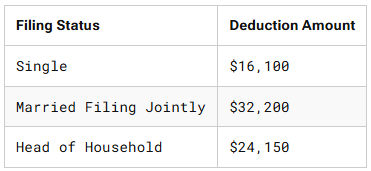

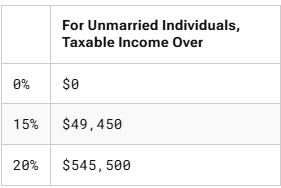

For this example we’ll use the 2026 single tax brackets (below) and standard deduction of $16,100

2026 Tax Brackets – Single Filers

2026 Standard Deduction

2026 Capital Gains Tax Brackets – Single Filers

For a quick example, let’s assume you have $30,000 in annual income.

- $30,000 annual income

- – $16,100 (standard deduction)

- = $13,900 taxable.

Using the charts above, we see you’re currently in the 12% tax bracket and the 0% capital gains tax bracket before making any withdrawals.

Step 3a – Determine Withdrawal Strategy that Minimizes Tax Burden

This step is more complex and depends on which of the Four Buckets you have to pull from. Generally, you should be pulling from your Taxable account. When you pull from your Taxable account, you are only taxed on any gain, not the principal. This keeps your tax bill lower than you might expect. Since you are under age 59.5 in this phase, you should avoid pulling from Tax-Deferred or Roth buckets as this will likely generate taxes and penalties.

Bucket Withdrawal Review

Following is a brief review of each bucket pertinent to this stage.

- Taxable – generally, this is your go to bucket for withdrawals. If you need to sell investments before withdrawing, you will pay capital gains tax on any gains (sale price – purchase price).

- Health Savings Account (HSA) – if your annual expenses include healthcare costs, consider pulling those costs from this bucket. Qualified withdrawals will not generate any taxes or penalties.

- Roth – avoid pulling from this bucket before age 59.5 if possible. Withdrawing gains generates both tax and penalty. While you can withdraw original contributions without tax or penalty, I suggest avoiding this just for the additional bookkeeping & reporting overhead.

- Tax-Deferred – avoid pulling from this bucket; taxes and penalties will apply before age 59.5 (exception: Roth conversions, see Step 3b)

If you need to sell investments in your Taxable account, you will pay capital gains on any increase in value (sale price – purchase price). Note that the capital gains brackets are much more generous. For a single-filer, you pay 0% on capital gains up to $49,450 total taxable income. Continuing our example above, you can realize an additional $35,550 in capital gains and still pay 0% tax.

Step 3b – Roth Conversions

If your income puts you below the 10% tax bracket (i.e. you’re paying 0 taxes) and you have money in a pre-tax bucket, consider doing a Roth conversion at least up to the point you fill up the standard deduction. Depending on how much pre-tax money you have, you may want to even consider doing Roth conversions into the 10% and 12% tax brackets.

Briefly explained, Roth conversions are a special tax loophole that allows you to convert money from Pre-Tax accounts to Roth accounts without penalty. However, you do pay income taxes. But if you’re below the 10% bracket, you could convert up to that bracket and effectively never pay income on that money or its earnings.

Important: Since Roth conversions count as regular income, make sure to consider impact to any capital gains realized from Step 3a.

Also Important: Roth conversions are beyond the scope of this article. There are other restrictions and rules to be aware of that may apply. Please research this in detail or talk to a tax professional before making any decisions.

Conclusion

Because of the wide range of possibilities and individual circumstances, it’s impossible to give any one strategy. The goal here is to equip you with the starting information to begin thinking through your personal situation. Take the time to gather the information outlined above and begin thinking about how you can minimize your tax burden. The effort is well worth it!