It’s a simple and harmless question. I’ve asked it and been asked it hundreds of times. It’s a great icebreaker. It’s a great way to get to know someone. The answer encompasses our identity, social status, and self-worth. After FIRE-ing, it can sting a little when asked. If you read my last post 018 | Life After FI: Six Months In – Happier, Anxious, and Still Figuring It Out, you know the question I’m talking about. It can really catch you off guard the first few times you’re asked. Be ready, because it’s only a matter of time before someone turns to you and asks:

“So, what do you do?”

Why It Stings

Actually, “sting” may not be the only word I’d use to describe the feeling when asked what I do after retiring early. Depending on the situation, I’ve felt: “awkward”, “guilty”, “embarrassed”, and “confused”, to name a few emotions. The first time someone asked, it just caught me totally off guard and I was momentarily confused while my brain stumbled to formulate a response: “uhmmmm… nothing, I guess… I’m sort of, well, I am retired”. On other occasions I’ve felt guilty for having the luxury of free time while others have to work (perhaps for the rest of their lives). And on other occasions I’ve felt awkward or embarrassed just because I’m in front of people I don’t know and I’m not comfortable disclosing that much about myself.

But recently I was asked and it stung a little. It stung even though I’ve already been asked a number of times. I should be past any discomfort, but apparently I’m not. I was attending a local AI Collective meetup on a Thursday night. Most of the crowd was there after work. It was full of people with strong, one-line answers to the question. “I’m a software engineer for X.” “I’m CTO at Y.” “I’m the founder at Z.” But me? I’m just there because I’m interested, as a hobby, exploring new things, to learn. I have no company, no project, no sales pitch, not even anywhere to be in the morning.

Then it happened — someone finally looked at me and asked “So, what do you do?”. My brain panicked and the negative thoughts rushed through it: “Oh crap, I don’t do anything”, “I’m going to seem like an idiot”, “These people are wasting their time talking to me”, “I no longer have any purpose or anything to offer”. And there is the sting — loss of identity. For the first time, I felt the full sting of losing my work identity, the identity I’d had for 30 years, MY one-liner. I managed to blurt something out about what I used to do and walked away feeling a little ashamed.

A New Phase of Life

The sting I experienced left me unsettled and feeling a little devoid of purpose. I’m now asking myself the question: “So, what do I do?”. After pondering this for a few days, I realized that the people in that AI Collective meeting are in a different phase of life than me. They’re still in their striving phase of life. They’re climbing, achieving, and acquiring. This phase of life is generally about having, doing, and achieving more.

I’m in a new phase of life now, different from the phase that my AI Collective friends are in. I’m searching for meaning, connection, and happiness. My phase of life is sort of about having and achieving less (or at least I should be, but that’s another topic). So, “retirement me” does have an identity and purpose. It’s just different from what “career me” had. Further, judging “retirement me” against the standards of “career me” is setting myself up for failure.

A New Answer to the Question

Since I am in a new phase of life, “what I do” isn’t missing; it’s just different. What I need, then, is a new answer to the question that aligns with my new priorities. This phase of life, I believe, is a quest for true and lasting happiness. And if you read 008 | Abundant Living: Giving and Receiving and 009 | Community: Life or Death / Boom or Bust, you know that “serving others” and “community” are critical to true happiness.

These two things go hand-in-hand. Community is about relationships. And serving others is a significant part of building relationships. The most important relationships to build are with my family first, close friends next, and then with others. Serving my family & friends happens on many levels/dimensions and it is much deeper and more involved than serving others. As such, the easiest way to describe my new purpose regarding family & friends is for me to just state my roles of “husband”, “father”, and “friend”. Serving others can happen in many ways, but my personal favorite is through encouragement. Today’s world of faceless communication like email, text, and social media is quick to tear people down. Encouragement is craved and needed more than ever.

So, the next time I’m asked “what do you do”, I have an answer that fits the pursuits of my new phase of life. I’ll likely tweak it to fit the situation, but I think I’ll answer (with a little humor) something like this:

I’m a husband, father, friend, and encourager. And I think you, my friend, are doing a great job!

Takeaway: You Have a New Purpose

What I’ve learned from this is that I haven’t lost my identity. I’ve left the building, achieving, and acquiring phase of life and entered a new phase focused on happiness, true purpose, and serving others. “What I do now” is different from “what I did then”. This experience has also reinforced to me that I’m on the right track by focusing on community and relationships. So, when you retire, be ready. What will your answer be to “the question”?

20 years ago, I bought a dream car. A 2004 Cobra Mustang in rare mystichrome paint. Rather than drive it, I mostly cherished it and kept it stored in perfect condition. My kids grew up around that car; I have pictures of them pre-school through college next to it. Fast forward to 2026 – it only had 10k miles on it and had become highly sought after by collectors. Four months after retirement I sold it. Not because I had to. Because retirement anxiety got loud enough that I felt compelled to.

Six months ago I made a well-thought-out, but imperfect, decision to retire and I’m still living with the weight of it. I am happier, but not without doubt. Read on for my honest evaluation of the experience so far.

Background – It Wasn’t a Perfect Exit

If you read my previous post 017 | The Decision to FIRE you already know I fast-tracked my retirement 3 years earlier than I was comfortable with. My employer of 15 years sold our small, family-like company to a private equity firm. And although the new firm treated me well, I was now in a high-stress, corporate environment. After 3 years of that, I decided to retire at age 59 even though I wasn’t 100% ready financially.

To make our numbers work and retire with the lifestyle we wanted, I really needed to work until age 62 according to my spreadsheet. The numbers technically worked at age 59, but they are dependent on: Social Security, Mrs. FIcology working 5 more years so we have healthcare, and Mrs. FIcology’s future pension. Also, in our favor, we are 100% debt-free and could sell our house if we had to.

If you’re following the stock market currently, you know it’s widely considered to be significantly over-valued (i.e. we’re due for a correction). And if you’ve been in the FI community for long, you also know that sequence of returns risk is the biggest threat to a new retiree’s portfolio. In other words, a major market correction in the first 5 or so years into retirement can completely wreck a retirement portfolio.

Despite all this, the numbers do work, and I had enough confidence to retire and free myself from my new corporate overlords.

The Negatives

Before deciding to retire, I did a ton of research and planning. Most importantly, I studied and reviewed our finances. I also did a number of deep dives on non-financial retirement topics. Topics ranging from time freedom to the phenomenon of early death from having no purpose. I felt fully prepared to expect and handle anything that would come my way. But, I was still surprised by my actual emotions & experiences.

Money Mind Games

The first thing that was really hard to accept is that I no longer had a paycheck coming in. We had a decent amount of cash built up in our bank account, and watching that dwindle instead of grow was much more difficult than I thought it would be. It was also difficult pulling from our investments for the first time to replenish our bank account. I became very focused on not spending money and questioning every expense. And there is a healthy level of that. But, I definitely crossed into unhealthy territory; I’m starting to loosen back up now.

Our savings has been another difficult thing for me. I’ve found myself checking the stock market daily. So much so that Mrs. FIcology can sometimes tell from my mood whether the market was up or down that day. About 4 months into retirement, the market took a brief nosedive of about 10-15%. This was MUCH harder to tolerate than I ever imagined. I didn’t panic sell; but it crossed my mind. Fortunately, I have an investment plan in place and I know better than to try to time the market. Nonetheless, it was still way more stressful on me than I thought it would be.

Even though I didn’t panic sell our investments, I did sell my Cobra Mustang as stated above. I make it a point not to live in regret, so I’m not regretful about it. But selling that was way harder than I expected. When the shipper loaded it up and left, I cried. Yeah… I know it’s dumb, but something that was a piece of my life for 20 years drove off that day.

Structure and Purpose Gap

The first time that someone asked me “What do you do?” it hit me harder than I expected. I’ve spent the last 30 years developing software and managing software teams. And now, I don’t do anything. “I’m retired.” Ouch. At the same time, my friends all continue to work. They have responsibilities, earn paychecks, invest, and are part of something larger. I don’t have any of that anymore.

The first few months of retirement, I was really busy. I created this blog website, wrote blog posts, caught up on things around the house, went to Bible studies, met people for coffee, and so on. I kept a rigorous schedule because that’s what I’ve done for the last 30 years. But now I’ve become less intentional about making lists and checking them off. I’ve been amazed at how quickly the days go by with me accomplishing so little. Don’t get me wrong; it’s great to do stuff at your own pace. But, the lack of structure can be unsettling and add to the feeling of lacking purpose.

Unexpected Emotions

While I knew being retired didn’t just automatically mean I’d be happy, I’ve experienced more negative emotions than I expected. I already mentioned some of my money & investment fears above. But I’ve found myself experiencing a really irrational fear — that we’ll live too long and run out of money. Seriously? I’m worrying about living too long? That’s some messed up, backwards, FI logic right there.

I don’t know if this counts as an emotion, but here’s another one. I find that the more free time I have, the more stingy I am with it. I’m less willing to go spend time with others or go do the things I said I’d do if I retired. Here’s an example: there’s a mountain bike trail about 45 minutes from us. I’ve always wanted to ride there, but I never did because it’s too much of a time commitment. I’ve been retired for 6 months and I’ve only gone one time. This one baffles me and I’m actively working to correct myself.

Boredom and loneliness are a couple other emotions I’ve experienced on occasion. While I’ve mostly kept these at bay, they do pop up occasionally. As a lifelong introvert and a survivor of severe depression, I know better than to let myself isolate. But without regular work interactions, it’s easier than ever to do.

Community / Friendship Fails

My biggest hope for retirement was to have more community and more friends. While I have made a few new friends, it’s nowhere near what I imagined. I knew how hard it is to make friends going into this, but it’s been much harder than even anticipated. I’ve joined 3 different men’s Bible studies. The one I was most hopeful for, I recently quit. After months of diligently attending, doing the studies, discussing, I had completely failed to make any meaningful contacts or friendships. A lot of that is my fault for being so introverted, but this group was also very introverted which makes it REALLY difficult to form a relationship.

So, I think I need to reframe my approach. While I haven’t thought through it in detail, I have some ideas. First, quickly evaluate groups/environments for their potential to build quality relationships. Some environments are not as well-suited and that’s okay. Determine that upfront and either try to make the environment that way or move on. Second, be more intentional forging friendships in groups. Don’t sit back and wait for people to come to me. Third, speak up and share sooner. I always wait until I’m comfortable to speak. By the time that happens, I’ve created an awkwardness that makes it even harder for me to talk. Fourth, offer to help others. Help people get what they want/need and they’ll help you. Finally, compliment and encourage others. Tell people when they say or do something you admire or that adds value.

The Positives

Okay, now for the fun part. I led with the hard stuff on purpose because the good stuff hits differently when you know the full picture. There’s a LOT of good stuff and it far outweighs the negatives.

Mental State

First of all is my overall mental state. I’m so much happier, calmer, and relaxed. I look forward to every single day. I don’t want to go to bed at night because I don’t want the day to be over. I’m kinder, more understanding, and more loving to my family and to others. When I was still working, I dreaded every single workday. I wasted my weekends being miserable because Monday was just around the corner. I would go for walks to clear my head and end up in tears because I was so miserable. Life is so much better now that I removed myself from that environment. I can’t even begin to tell you how huge this is for me. I’m so thankful for my life now.

Marriage

My improved mental state and my new time freedom have allowed great improvements to Mrs. FIcology’s and my relationship. Not only am I kinder and more patient, I have the time and energy to serve her more. It’s been great to take on more chores and perform more acts of kindness. One of my favorite things to do is to prepare dinner for her each night and clean up afterwards. She’s done that for our family for years and now it’s my turn to do it for her.

Planning for retirement and being retired have also made me much more conscious of the limited time each of us has. That makes me appreciate my time with Mrs. FIcology even more and be less likely to waste any on petty arguments and such. We still have our own interests and spend time separately, but we rarely waste any time being angry at each other.

Community / Friendship Wins

While I’ve had some failures in this department (see above), I’ve also had some wins. I’ve made a few new guy friends and strengthened bonds with a handful of others. I’ve grabbed coffee with friends that I previously didn’t have time for. I created my own 8-week Bible study, including the material, and hosted it along with Mrs. F. We made a couple new friends out of that and strengthened some existing friendships.

Mrs. F. and I have joined a local ChooseFI group that we attend monthly. We’ve made new acquaintances through the group. And it has helped with some of my money fears above. It’s also been useful to hear others’ experiences and perspectives on FIRE topics.

And I’ve joined a monthly, local AI group. It has helped me learn AI and continue to explore technology. I’ve also made some new contacts that may let me turn this hobby into some cash. This helps me with my sense of purpose struggles I mentioned above (and it may help with my money fears if it generates some income).

Knowledge / Experimentation

One of the most rewarding things about retirement is the time and freedom to pursue new knowledge. It’s honestly been a challenge to give myself permission to pursue learning things that “work me” would never have budgeted time for.

I mentioned above that I’ve joined a local AI group. But I’ve also spent a fair amount of time learning and applying AI. As a lifelong software developer and technology enthusiast, AI fascinates me. While I’m still in my infancy learning it, I’ve used it to: rebalance our portfolio, grammar check blog posts, create a job search application for my son, generate code for a side hustle gig, and more. I’ve found this to be very satisfying and it gives me a sense of purpose.

I’ve been a self-help junkie most of my life and being retired has allowed me to continue that trend. But, it’s also allowed me to give myself permission to read and learn other things. For example, I just read “Alice’s Adventures in Wonderland” and “Through the Looking Glass”. I’ve never really allowed myself the time to read fiction before. Another example of allowing myself to be curious for curiosity’s sake is a recent deep dive I did into Euler’s number. Euler’s number is an irrational constant, like Pi, that represents continuous growth. In the FI world, it can be used to calculate continuous compounding of interest. As a FI/FIRE enthusiast, I found this super interesting.

Experiences

Being retired this short time has enabled a number of experiences for us that we would never have had if I was still working full-time. I’ll list just a few.

Our 30th anniversary was in March and we took a trip to San Antonio for a week. We stayed on the river walk downtown. We got a VIP tour of the Alamo including items in their private vault that few people get to see. We visited all the mission sites there, caught up with some old friends, saw a spectacular light display, and a bunch of other touristy stuff.

Our son graduated college a couple weeks ago and was home briefly before landing his first job. The day before he left, we hiked a long trail that ends at a wet weather set of waterfalls. The hike was tough but the falls were absolutely amazing. Words can’t describe the majesty of rushing waterfalls in the middle of lush green woods while dangling my feet in the cold clear water. What a great way to spend our son’s last day with us. If not for retirement, I don’t know that I would have had the time or energy to do that hike.

Later this summer, Mrs. F and I are going to work in a fireworks stand. We will get paid for our time (not a lot), but we’re in it for the experience, not the money. It’s a chance to meet other people, serve the family that owns the fireworks stand, and serve the people of our community that shop there. And because we’re doing that, we got invited to a free evening of games, food, and an awesome fireworks show from the local distributor. That show was one of the neatest experiences we’ve had recently.

Still Figuring It Out – And That’s Okay

Overall, retirement has been great. Many of my expectations have been met and others have not. There have been good and bad surprises. I honestly expect all of retirement to be this way: to continue learning and doing new things, to have ups and downs, and to continue chasing what brings us happiness. I recently heard a podcast with Martha Beck that really struck a chord with me. So much so that I think it will be the mantra for my entire retirement. That is: to methodically and consistently move towards things/people/experiences that bring true life joy (not to be confused with quick dopamine hits like shopping, food, social media, etc.) and away from those things that do not. It’s a simple concept, but may be difficult in practice especially when shedding things that steal joy. Thanks for reading and may your path be joy-filled, friend.

Welcome back (or just “welcome” if this is your first read). I’m the Professor here at FIcology 101 and I want to share with you probably the hardest decision of my life – the decision to retire (or to “FIRE” if we’re using community lingo).

Introduction

While my life goal has been to retire at age 59 (which I did, congratulations to me), my “can I really do this” path felt like 62 was more realistic. And honestly, I really wanted to wait it out and hit that more realistic target, giving me a more financially-abundant retirement. But that wasn’t in the cards, and this story illustrates why being on the FI path is so powerful.

From Happy to Unhappy Employment

After starting life over with my family in the semi-rural midwest, I was fortunate enough to land a software development position with a small and up-and-coming SaaS company. As the company grew over the next 14 years, so did my role, position, responsibilities, and salary. The owners legitimately cared about the employees, encouraged and grew us, and maintained a very family-like atmosphere. After years in the large and impersonal corporate world, I finally found my home. Or so I thought…

In my 15th year with them, the company was acquired by a private equity firm. And while the new company treated me fairly and didn’t do anything “wrong”, I was unwillingly back in the corporate world again. This wasn’t the job I was hired for and it wasn’t the family-like environment that I loved. I found myself: constantly stressed, dreading every day, and frequently in tears over how unhappy I was.

Looking back, it’s shocking how fast your life and plans can get uprooted. If I hadn’t already been on the path to FI, things could have been much worse for me.

The Fire Fueling My FIRE

The next few years with the new company lit a fire under my FIRE plans. At first I was hopeful this new company would work out despite the enormous changes, culture shifts, and chaos. Unfortunately it became clear after about a year that it was never going to be. So, I decided to step up my FIRE plans and timeline. I’d already been on the path to FI for years, but how close was I to FIRE and could I pull it off sooner?

Step 1 – Fast Track My FI Education

The first thing I did was start consuming every podcast and book I could get my hands on. I devoured books on “early retirement”, “financial freedom”, “tax planning”, and more. Here are some books that helped me:

The Simple Path to Wealth – JL Collins

Find Your Freedom – Jamie Hopkins and Ron Carson

How Much Money Do I Need to Retire – Todd Tresidder

The Success Principles – Jack Canfield

The 5 Years Before You Retire – Emily Guy Birken

The Psychology of Money – Morgan Housel

I also had FI/FIRE and related podcasts playing in my earbuds and in the car constantly. There are a lot of podcasts to choose from. Here are some of my favorites:

ChooseFI

Mile High FI

The Financial Independence Show

Your Money Guide on the Side

Forget About Money

Podcasts and books not only increased my knowledge, they also inspired me to do independent research. The more I learned, the more the pieces began to fall together, and the more of a reality the possibility of FIRE-ing became.

Step 2 – Gather Expenses & Cost of Living

There’s no way to determine if you can retire without knowing your actual annual living expenses. I spent a significant amount of time reviewing our checkbook, utility bills, credit card statements, tax receipts, and so on. I captured all of this data into broad categories at the annual level. Expenses aren’t all smooth and predictable; they appear in spikes and at random. I had to estimate allowances for unpredictable items like: auto repairs, HVAC repairs, and so on. Your categories will likely be different from mine. For example, we’re fortunate to not have a car payment at this time. These are the categories I used:

Health Insurance

Personal Property Taxes

Auto Insurance

Groceries

Utilities – Electric, Propane, Trash, Internet

Church / Charity

Cell Phone

Automobile (maintenance, depreciation)

Dental

Medical – Out of Pocket

Home Property Tax

Home Insurance

Home Maintenance

Miscellaneous – group for all other routine spending (gas, dining out, entertainment, etc…)

Safety Buffer – a configurable percentage (I used 10%) of the sum of all the above expenses. For example, if the above expenses totaled $50,000 per year, then this would add $5,000 to my total expenses.

Important: I can’t stress enough the importance of being thorough here. Missing expenses in this step could lead you to make a disastrously wrong decision. Be sure to account for non-monthly and non-recurring expenses.

Step 3 – Gather Assets

For us, this is simply a list of our retirement accounts broken down by bucket type (Tax-Deferred, Roth, Taxable, and HSA). Knowing the bucket type allows you to factor in tax consequences. Withdrawals from tax-deferred will be taxed as normal income (and penalized if you’re under age 59.5), for example.

Note: While it’s important to know the equity in your home and autos, I did NOT include these as part of our retirement assets for this exercise. We plan to live in our home and drive our cars. If we were selling our home (downsizing, for example), then I might include some of that equity here.

Step 4 – Homegrown Excel Forecast Spreadsheet

For years I’ve had a very simple online financial calculator that I’d used. While that was great for tracking our FI progress, it was not sufficient to make a decision this important. So, I built my own version of a forecast / drawdown spreadsheet. I factored in things like Social Security, interest rates, tax rates, inflation rates, Mrs FIcology’s pension, and so on. It allowed me to play with all the numbers and see how long our money lasts under different scenarios. I spent hours upon hours in this spreadsheet adding new features and comparing different withdrawal strategies. If you’ve been around the FI community much, you know many of us have our own spreadsheet like this. This was the foundation of my decision on when I could pull the trigger and retire.

Step 5 – Financial Advisor

To make sure I wasn’t missing anything, I enlisted the help of a financial advisor. I provided him with all of our info (which was easy because I’d already gathered it above), and he reviewed and ran it through his firm’s software package that runs your numbers through a Monte Carlo simulator to determine the odds of your assets lasting through retirement. The result: he confirmed what my Excel sheet had already told me. I could retire.

Note: I suggest finding a flat-fee/fee-only advisor as opposed to an AUM (assets under management) advisor. The latter manages your portfolio in return for a percentage of it as an annual fee.

Step 6 – Monte Carlo Simulator

As one last sanity check, I used an online Monte Carlo simulator to enter in all of our numbers and run a number of scenarios and tests. If you haven’t played with one of these, it’s worth doing. Once you’ve input your assets, you can simulate all kinds of scenarios, periods of history, worst case, best case, and so much more. The one I used is projectionlab.com. At the time, you could sign up for a free trial which was plenty for me to confirm one more time that I could retire. At some point, I may go back and purchase a membership so that I can continue monitoring our chances of survival.

Step 7 – Deep Breath and Take the Plunge

For a few months I continued to work at the job I didn’t like. It continued to NOT be what I wanted and the morale there continued to decline. I won’t go into details, but suffice it to say that one day came where I finally had enough. The hit to my happiness was no longer worth the paycheck. So, I reconfirmed plans with Mrs FIcology and put in notice. Work took the news well and I actually gave 6 weeks notice and trained my replacement. I left on amicable terms and I’m thankful for that.

Conclusion

That’s how my decision to FIRE went down. It has been a huge relief and I am enjoying life again. But, here’s what I can tell you six months later: retiring didn’t solve everything, and it surfaced a few things I wasn’t prepared for. The next post is the honest version of what life after FIRE actually looks like. See you there.

Welcome back! We’re wrapping up our four-part series on tax bracket arbitrage (TBA). In Part 1, we introduced tax bracket arbitrage and the tools available. In Part 2 we discussed the accumulation stage of your FIRE journey. In Part 3 we discussed early/partial retirement and here we’ll talk about the full retirement phase.

Writing this series has been an eye-opener for me. The base concepts are relatively simple. But the number of variables to consider (age, marital status, income level, tax brackets, mix of different savings buckets, etc…) makes strategizing complex. The number of possible scenarios is seemingly infinite. It’s been challenging to provide useful and actionable information while maintaining a simple and digestible format to fit the potentially vast variety of readers.

Full Retirement Stage

For our purposes, we’ll define full retirement as any time after age 59.5 that you leave full-time employment/wages. While you may choose to supplement your income with part-time work or other income, you’re likely drawing down your retirement nest egg. The significance with age 59.5 is that this is when you can withdraw from tax-deferred retirement accounts without penalty (in the U.S.).

The goal in this stage is to enjoy life and make your savings last the rest of your life while minimizing present and future tax burden. Like all stages, each person will have their own unique situation, savings, investments, and spread across the 4 main buckets. This means your specific strategies will be unique to you.

TBA Strategies

Similar to the early retirement stage, in this stage of the FIRE journey we’re all in unique and very different situations. As before, there’s no one-size-fits-all strategy, here are multiple facets to consider, and we’ll keep it simple here. In many ways, the strategies are the same/similar as for early retirement. The main difference is that, because we’re aged 59.5 or later, we have access to our tax-deferred buckets without penalty.

Gathering Data

Before we start, you’ll need to gather the following info. (This is the same info we gathered Part 3, repeated here for convenience.)

Annual income sources and amounts. In order to have a strategy, you absolutely must know all your income sources (wages, interest, dividends, etc.) and be able to project those amounts each year with reasonable accuracy. Unlike the early retirement phase, you may also have pension or social security in this phase. Include those as well. Do NOT include retirement savings drawdowns in this number.

Savings balances by bucket type. Because each bucket type has its own tax rules, summarize your savings amounts by bucket type. See The Four Buckets for more information.

Applicable U.S. income tax brackets. The simplest way is to just use google. Search “2026 US tax brackets”, for example. Don’t forget state taxes, if applicable.

Applicable U.S. capital gains tax brackets. Long-term capital gains (gains on investments held more than 1 year) are taxed differently than short-term capital gains (gains on investments held 1 year or less). Note: qualified dividends are also taxed at long-term capital gains rates; that discussion is beyond the scope of this article.

Applicable U.S. standard tax deduction. Again, just use google to find this. Note: If you itemize deductions (very few people do thanks to generous standard deductions), use your total itemized deductions instead.

Annual lifestyle expenses. This may be the toughest data to get, but it’s worth it. Estimate your annual expenses by category, if possible. At minimum group into discretionary and non-discretionary.

Strategy

The strategy in full retirement is largely the same as the early retirement phase. The process below will need to be repeated annually. Life is always changing and each year will have unique expenses, incomes, tax brackets, and so on.

Step 1 – Calculate Required Annual Drawdown

Calculate the amount you’ll need to pull from your savings. This is simply the difference between your total annual income and your annual lifestyle expenses.

Note: if your annual income sources include things that will not be used as income (example dividends that are set to reinvest), exclude those from the total annual income.

Annual Drawdown = Annual lifestyle expenses – Annual income

Step 2 – Determine Marginal Income and Capital Gains Tax Brackets

Using your annual income, applicable tax brackets, and applicable standard deduction, find your marginal tax rate(s). For more info see our post on Marginal vs Effective Tax Rates.

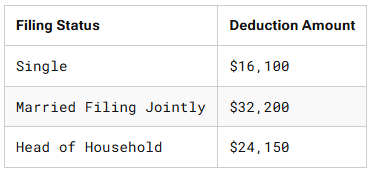

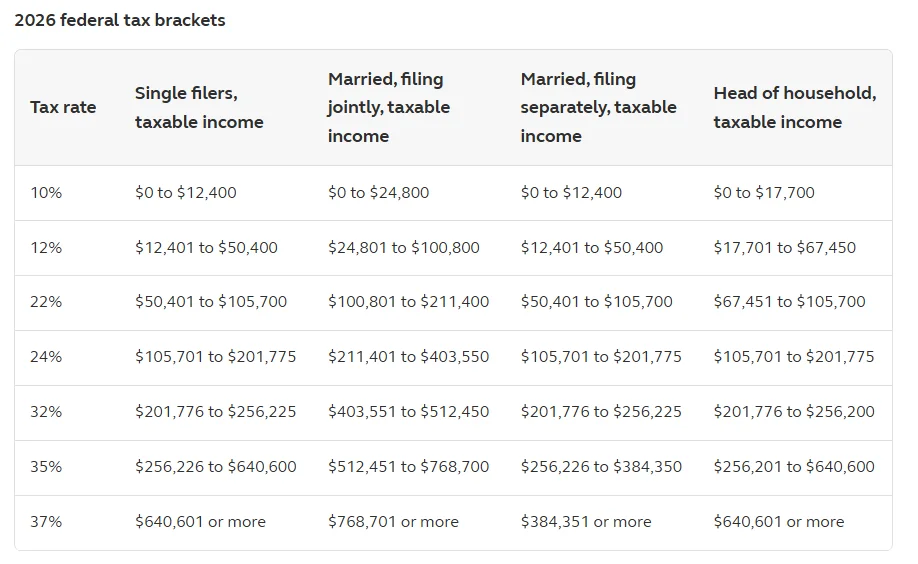

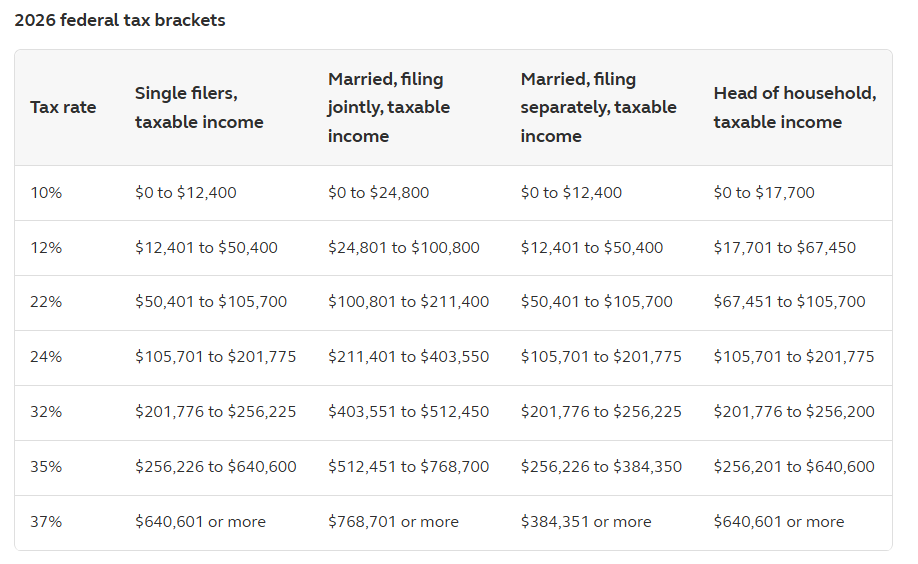

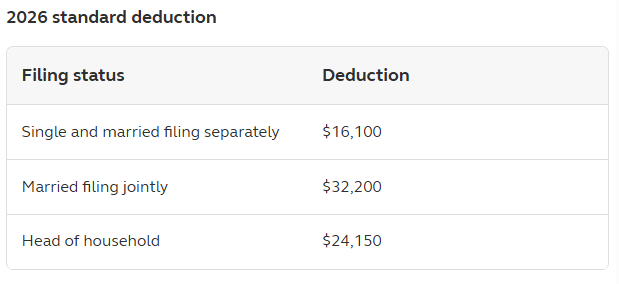

For this example we’ll use the 2026 single tax brackets (below) and standard deduction of $16,100

2026 Tax Brackets – Single Filers

2026 Standard Deduction

2026 Capital Gains Tax Brackets – Single Filers

For a quick example, let’s assume you have $30,000 in annual income.

$30,000 annual income

– $16,100 (standard deduction)

= $13,900 taxable.

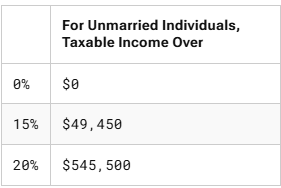

Using the charts above, we see you’re currently in the 12% tax bracket and the 0% capital gains tax bracket before making any withdrawals.

Step 3a – Determine Withdrawal Strategy that Minimizes Tax Burden

This step is more complex and depends on which of the Four Buckets you have to pull from. Generally, you should be pulling from your Tax-Deferred account to the point you are in a low/no tax bracket. This has 2 benefits: first it gets your money out with little to no taxes and second, it reduces potential RMDs (Required Minimum Distributions) later. Next, pull from your Taxable account — you are only taxed on any gain, not the principal. Since Roth accounts are tax free forever, only pull enough from there to meet your needs while keeping taxes low from Tax-Deferred and Taxable account withdrawals.

Bucket Withdrawal Review

Following is a brief review of each bucket pertinent to this stage.

Tax-Deferred – money pulled from here is taxable as normal income. So, prioritize pulling from here, but only if you’re in a lower tax bracket. (Optional: you can do Roth conversions instead of pulling the money out, see Step 3b)

Taxable – this is likely your 2nd goto bucket for withdrawals. But, if you need to sell investments before withdrawing, you will pay capital gains tax on any gains (sale price – purchase price). Only do this if you’re in a favorable capital gains tax bracket.

Roth – this is likely your 3rd goto bucket. Withdrawals from here are now 100% tax & penalty free. Use this just enough to keep the amounts pulled from Tax-Deferred & Taxable accounts low enough to minimize taxes.

Health Savings Account (HSA) – if your annual expenses include healthcare costs, consider pulling those costs from this bucket. Qualified withdrawals will not generate any taxes or penalties.

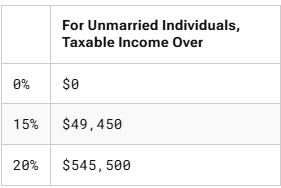

If you need to sell investments in your Taxable account, you will pay capital gains on any increase in value (sale price – purchase price). Note that the capital gains brackets are much more generous. For a single-filer, you pay 0% on capital gains up to $49,450 total taxable income. Continuing our example above, you can realize an additional $35,550 in capital gains and still pay 0% tax.

Pro Tip: Since you’ll likely start getting Social Security benefits in this stage of life, it’s important to note that those benefits count as income (although they are taxed differently). In 2026, the average Social Security benefit is approximately $2,071 per month. If this is your only income, you are effectively starting the year with roughly $24,852 already ‘filling’ your 0% and 10% tax zones. Always check your Social Security taxability before deciding how much to pull from other buckets.

Step 3b – Roth Conversions

If your income puts you below the 10% tax bracket (i.e. you’re paying 0 taxes) and you have money in a pre-tax bucket, consider doing a Roth conversion at least up to the point you fill up the standard deduction. Depending on how much pre-tax money you have, you may want to even consider doing Roth conversions into the 10% and 12% tax brackets.

Briefly explained, Roth conversions are a special tax loophole that allows you to convert money from Pre-Tax accounts to Roth accounts without penalty. However, you do pay income taxes.

But if you’re below the 10% bracket, you could convert up to that bracket and effectively never pay income on that money or its earnings.

Important: Since Roth conversions count as regular income, make sure to consider impact to any capital gains realized from Step 3a and any other withdrawals from Tax-Deferred accounts.

Also Important: Roth conversions are beyond the scope of this article. There are other restrictions and rules to be aware of that may apply. Please research this in detail or talk to a tax professional before making any decisions.

Step 3c – Consider RMDs

RMDs are Required Minimum Distributions from your Tax-Deferred accounts. It’s Uncle Sam’s way of making sure he gets his tax money. Beginning at age 73 or 75 (depending on your birthdate), the government requires you to begin pulling a % from your tax-deferred accounts on a schedule that they determine. The gotcha here is that if you have a lot in tax-deferred accounts, this can force you into a higher tax bracket. Therefore, it behooves you to be thinking about this ahead of time to consider withdrawing from these accounts sooner, while you can control the tax bracket, rather than later where Uncle Sam forces your hand.

NOTE: RMDs are beyond the scope of the article, but mentioned here for completeness.

Conclusion

Because of the wide range of possibilities and individual circumstances, it’s impossible to give any one strategy. The goal here is to equip you with the starting information to begin thinking through your personal situation. Take the time to gather the information outlined above and begin thinking about how you can minimize your tax burden. The effort is well worth it!

Congratulations on completing the 4-part series! This has been a learning experience for me and I hope it has been for you. There is a lot of complexity in retirement tax planning and strategies are heavily dependent on individual situations. You’re now equipped with the necessary concepts to put together your own plan.

Welcome back! We’re continuing our four-part series on tax bracket arbitrage (TBA). In Part 1, we introduced tax bracket arbitrage and the tools available. In Part 2 we discussed the accumulation stage of your FIRE journey. And here we’ll talk about the early/partial retirement phase.

Early/Partial Retirement Stage

For our purposes, we’ll define early/partial retirement as any time before age 59.5 that you leave full-time employment/wages. This could be full retirement or it could mean part-time work to fill your time or supplement your lifestyle. You’re tapping into your savings, rather than actively adding to them. The significance with age 59.5 is that this is when you can withdraw from tax-deferred retirement accounts without penalty (in the U.S.).

The goal in this stage is to enjoy life while minimizing present and future tax burden. Like all stages, each person will have their own unique situation, savings, investments, and spread across the 4 main buckets. This means your specific strategies will be unique to you.

TBA Strategies

At this stage of the FIRE journey, we’re likely all in unique and very different situations. So, more than ever, there’s no one-size-fits-all strategy. Also, there are multiple facets to consider. We’ll keep it simple here.

Gathering Data

Before we start, you’ll need to gather the following info:

Annual income sources and amounts. In order to have a strategy, you absolutely must know all your income sources (wages, interest, dividends, etc.) and be able to project those amounts each year with reasonable accuracy. Do NOT include retirement savings drawdowns in this number.

Savings balances by bucket type. Because each bucket type has its own tax rules, summarize your savings amounts by bucket type. See The Four Buckets for more information.

Applicable U.S. income tax brackets. The simplest way is to just use google. Search “2026 US tax brackets”, for example. Don’t forget state taxes, if applicable.

Applicable U.S. capital gains tax brackets. Long-term capital gains (gains on investments held more than 1 year) are taxed differently than short-term capital gains (gains on investments held 1 year or less). Note: qualified dividends are also taxed at long-term capital gains rates; that discussion is beyond the scope of this article.

Applicable U.S. standard tax deduction. Again, just use google to find this. Note: If you itemize deductions (very few people do thanks to generous standard deductions), use your total itemized deductions instead.

Annual lifestyle expenses. This may be the toughest data to get, but it’s worth it. Estimate your annual expenses by category, if possible. At minimum group into discretionary and non-discretionary.

Strategy

The process below will need to be repeated annually. Life is always changing and each year will have unique expenses, incomes, tax brackets, and so on.

Step 1 – Calculate Required Annual Drawdown

Calculate the amount you’ll need to pull from your savings. This is simply the difference between your total annual income and your annual lifestyle expenses.

Note: if your annual income sources include things that will not be used as income (example dividends that are set to reinvest), exclude those from the total annual income.

Annual Drawdown = Annual lifestyle expenses – Annual income

Step 2 – Determine Marginal Income and Capital Gains Tax Brackets

Using your annual income, applicable tax brackets, and applicable standard deduction, find your marginal tax rate(s). For more info see our post on Marginal vs Effective Tax Rates.

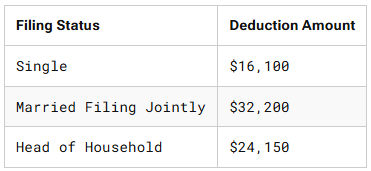

For this example we’ll use the 2026 single tax brackets (below) and standard deduction of $16,100

2026 Tax Brackets – Single Filers

2026 Standard Deduction

2026 Capital Gains Tax Brackets – Single Filers

For a quick example, let’s assume you have $30,000 in annual income.

$30,000 annual income

– $16,100 (standard deduction)

= $13,900 taxable.

Using the charts above, we see you’re currently in the 12% tax bracket and the 0% capital gains tax bracket before making any withdrawals.

Step 3a – Determine Withdrawal Strategy that Minimizes Tax Burden

This step is more complex and depends on which of the Four Buckets you have to pull from. Generally, you should be pulling from your Taxable account. When you pull from your Taxable account, you are only taxed on any gain, not the principal. This keeps your tax bill lower than you might expect. Since you are under age 59.5 in this phase, you should avoid pulling from Tax-Deferred or Roth buckets as this will likely generate taxes and penalties.

Bucket Withdrawal Review

Following is a brief review of each bucket pertinent to this stage.

Taxable – generally, this is your go to bucket for withdrawals. If you need to sell investments before withdrawing, you will pay capital gains tax on any gains (sale price – purchase price).

Health Savings Account (HSA) – if your annual expenses include healthcare costs, consider pulling those costs from this bucket. Qualified withdrawals will not generate any taxes or penalties.

Roth – avoid pulling from this bucket before age 59.5 if possible. Withdrawing gains generates both tax and penalty. While you can withdraw original contributions without tax or penalty, I suggest avoiding this just for the additional bookkeeping & reporting overhead.

Tax-Deferred – avoid pulling from this bucket; taxes and penalties will apply before age 59.5 (exception: Roth conversions, see Step 3b)

If you need to sell investments in your Taxable account, you will pay capital gains on any increase in value (sale price – purchase price). Note that the capital gains brackets are much more generous. For a single-filer, you pay 0% on capital gains up to $49,450 total taxable income. Continuing our example above, you can realize an additional $35,550 in capital gains and still pay 0% tax.

Step 3b – Roth Conversions

If your income puts you below the 10% tax bracket (i.e. you’re paying 0 taxes) and you have money in a pre-tax bucket, consider doing a Roth conversion at least up to the point you fill up the standard deduction. Depending on how much pre-tax money you have, you may want to even consider doing Roth conversions into the 10% and 12% tax brackets.

Briefly explained, Roth conversions are a special tax loophole that allows you to convert money from Pre-Tax accounts to Roth accounts without penalty. However, you do pay income taxes. But if you’re below the 10% bracket, you could convert up to that bracket and effectively never pay income on that money or its earnings.

Important: Since Roth conversions count as regular income, make sure to consider impact to any capital gains realized from Step 3a.

Also Important: Roth conversions are beyond the scope of this article. There are other restrictions and rules to be aware of that may apply. Please research this in detail or talk to a tax professional before making any decisions.

Conclusion

Because of the wide range of possibilities and individual circumstances, it’s impossible to give any one strategy. The goal here is to equip you with the starting information to begin thinking through your personal situation. Take the time to gather the information outlined above and begin thinking about how you can minimize your tax burden. The effort is well worth it!

Welcome back! We’re continuing our four-part series on tax bracket arbitrage (TBA). In Part 1, we introduced tax bracket arbitrage and the tools available. In parts 2 through 4 we’ll cover the strategies for each of the major Life Stages: Accumulation, Early/Partial Retirement, and Full Retirement. In this post, we’re focusing on the first: Accumulation Stage.

Accumulation Stage

The Accumulation Stage of your FI journey is the first stage. It’s the early phase of life where you’re probably working full-time, earning the most money, and subsequently paying the highest taxes. The goal in this stage is to save as much as possible while still enjoying life. Each person will have their own balance of saving vs consuming that they’re comfortable with.

Why this Stage is Critical

Even though retirement may seem like a far-away dream, this is the most critical stage of your journey for retirement. These are the years that determine, by the actions you take, how well your retirement will be (or if you even retire at all). These are also the years that allow you to take full advantage of the power of compounding. See “The Time Tax / Cost of Delay” section of our previous blog post: The Urgency of Now to understand the importance of compounding.

Key Assumption

Tax bracket arbitrage (TBA) at this stage of the FI journey is based on a single important assumption.

Assumption: You will likely be in a lower tax bracket during retirement than you are now, due to these early years being your highest earning years.

While this assumption will be true for most of us, there are some things that could make that NOT true for you. Some of these include:

Already in a low tax bracket: for whatever reason – your earnings are low, you file taxes as married but only one of you works, etc.

U.S. raises taxes in the future: this seems unlikely since politicians who do so tend not to get re-elected. But, the U.S. is currently facing unprecedented federal debt that will have to be dealt with at some point.

Spousal death or divorce: this would move you from married tax brackets (more favorable) to single tax brackets (less favorable). This is often referred to as “the widow’s tax”.

Inheritance or other income: you may have inheritance, pension, or some other taxable income in retirement that keeps you in a higher tax bracket.

TBA Strategies

Your strategy will likely be a mix that’s personal to you. There’s no one-size-fits-all answer. However, there are some consistent fundamental principles to keep in mind as you design your personal strategies.

Common Strategy Principles

The following principles hold true regardless of the TBA strategy you choose:

Save as much as reasonably possible. We’ve covered this multiple times, but it’s worth repeating; it’s the single most impactful lever you have to pull and it has a double-effect:

It accelerates your savings. The more you save, the sooner you reach FI.

It keeps your living expenses low. The less you learn to live on, the less you need to be FI, and the sooner you reach FI.

Always take full advantage of your employer’s retirement plan matching. This is free money. At minimum, always contribute enough to maximize your employer’s match before directing savings anywhere else.

Have an emergency fund. Buildup six months of living expenses in safe, post-tax accounts like high-yield savings or laddered CDs. This gives you peace of mind and options in the case of job loss or other catastrophe.

Utilize all four buckets if possible. Having savings in each of Tax-deferred, Roth, Taxable, and HSA accounts gives you the most flexibility for life AND tax bracket arbitrage.

Strategy

The general strategy can be summarized as follows: Defer taxes on any income that’s in a higher marginal tax bracket than your effective retirement tax rate. The larger the difference between these two, the more advantageous this strategy becomes.

NOTE: Why compare our current marginal tax rate to our retirement effective tax rate? Because when we defer taxes on current earnings, we are deferring taxes in the top bracket (i.e. our marginal tax rate). This same money withdrawn at retirement will be spread across all the tax brackets (i.e. our effective tax rate).

Gathering Data

Your current marginal tax bracket is easy—use your current income and the table of federal tax brackets below. Your retirement tax bracket is tougher to determine. To estimate that, you’ll need the following data:

Your annual retirement lifestyle expenses. This will likely change as life and priorities change; just do your best estimate given what you currently know and plan. It represents how much you’ll be pulling from your retirement accounts.

The U.S. tax brackets at retirement. We don’t know the future; I suggest you use the current tax brackets for simplicity.

How much of your retirement savings will be tax-deferred. This is a bit of a chicken-and-egg situation. How much you tax-defer depends on your expected retirement tax bracket and your retirement tax bracket will depend on how much you tax defer.

Effective tax rate calculation. See our post on Marginal vs Effective Tax Rates for how to do this. NOTE: for simplicity, you could use your marginal retirement rate instead. That will give you a lower estimate of potential tax savings; but if it gets you to do this exercise, it’s well worth it. Personally, I’d suggest you do it both ways (with marginal and effective retirement tax rates) for a thorough understanding of these concepts.

Bucket Contribution Order

You’ll remember from Blog Post 012 that our four investment buckets are: Tax-Deferred, Roth, HSA, and Taxable. All of these have contribution limits with the exception of taxable, obviously. So, as you contribute to these to defer taxes, you may hit these limits while still having more savings to invest. Here’s the rough order to contribute for retirement as you hit the maximums:

Tax-Deferred – 401(k), 403(b), Traditional IRA

Roth – Roth IRA, Roth 401(k)

HSA – Health Savings Account

Taxable – Individual or Joint Brokerage accounts

You need not max out one bucket before contributing to another. There is no one-size-fits-all strategy here. For example, it may be wise to put some into an HSA for possible health issues even before you’ve maxed out Tax-Deferred and Roth. Alternatively, you may want to switch the order of HSA and Roth, to defer the absolute most income.

Alternate Strategy – If Your Retirement Tax Rate is NOT Lower

If you’re one of the few that will have more income in your retirement than you have now, you may want to skip some contributions to the Tax-Deferred and instead focus on Roth, HSA, and Taxable.

Alternate Bucket Contribution Order

HSA – never taxable if used for healthcare

Roth – although this is post-tax contributions, the gains & interest are never taxable

Taxable – don’t underestimate the power of a taxable account. Capital gains and qualified dividends are taxable, but at the much lower “Capital Gains Tax Rate”. Further, capital gains grow tax-free until you decide to sell.

Tax-Deferred – This is likely still a valuable bucket for you depending on your circumstances. IMPORTANT: if your employer matches contributions to this type of account, you should be contributing enough to get that full match in this bucket before contributing anywhere else.

Conclusion – Call to Action

In the accumulation stage of your FI journey, your goal is to save as much as possible. That includes using TBA to supercharge the impact of those savings. The TBA goal is: Defer taxes on any income that’s in a higher marginal tax bracket than your effective retirement tax rate.

Everyone’s situation is different and everyone has different priorities. It would be impossible to come up with a single strategy to fit everyone. The goal here is to increase your understanding so that you can design strategies that work for you. Use the information here to:

Determine your current marginal tax rate

Determine your retirement effective tax rate

Use a spreadsheet or other tool to play “what if” scenarios with different contribution amounts and retirement withdrawal amounts.

Remember:

Tax-Deferred bucket contributions reduce your taxable income which may lower your current marginal tax rate.

Roth bucket withdrawals are not taxable in retirement, so these accounts will lower your retirement effective (and marginal) tax rate.

One final consideration: Tax-Deferred savings generally have RMDs (Required Minimum Distributions). That means starting at some age, the government will require you to start taking taxable distributions from these accounts. This can force you into higher tax brackets in retirement. Be sure to research RMDs and consider them in your retirement planning.

What if I told you that two people could earn the exact same amount of money over their lifetime, but one of them pays 30% less in taxes simply by changing when they claimed and how they pulled that income? Interested? If so, read on!

What is Tax Bracket Arbitrage?

We know what tax brackets are from our earlier post on Marginal vs Effective Tax Rates. So let’s start with a definition of “arbitrage”. Dictionary.com defines arbitrage as follows:

arbitrage NOUN

Finance. The purchase of currencies, securities, or commodities in one market for immediate resale in others in order to profit from unequal prices.

For “Tax Bracket Arbitrage”, instead of “currencies, securities, or commodities”, we’re talking about taxable income and instead of “markets”, we’re talking about tax brackets. So we can write our definition as:

tax bracket arbitrage

The strategic use of different account types, income classifications, and timing to move money from high-tax “zones” to low-tax (or no-tax) “zones”.

That sounds great except that you can’t just directly choose a lower tax bracket. You can, however, strategically use the various tax breaks, savings vehicles, and varying income levels at different stages of life to shift income to more preferential tax brackets. This can result in HUGE tax savings with minimal effort. In the most simplistic form, we’re manipulating when and how we take our income so that it’s in the lowest possible tax bracket when taxes become due.

IMPORTANT: We’re focusing on U.S. tax brackets and laws here. Many countries work similarly, but anything non-U.S. is outside the scope of this discussion.

Our Toolbox – The Four Buckets

The main tools at our disposal for tax bracket arbitrage are the four types of investment account types:

Tax-Deferred

Roth

Taxable

Health Savings Account (HSA)

See our previous blog post on The Four Buckets for a detailed discussion of each.

NOTE: Make sure any account type you utilize allows you to choose how you invest the money deposited (as opposed to simple interest-bearing or other poor investment vehicles). This is generally true nowadays, but check your specific accounts to be sure. The last thing you want is your money NOT to grow, or worse, lose value to inflation.

Why This Matters Now (2026 Context)

Since we are in 2026 and the One Big Beautiful Bill Act (OBBBA) has made the 2017 Tax Cuts and Jobs Act (TCJA) brackets permanent, we have a stable playing field to plan these strategies for decades to come.

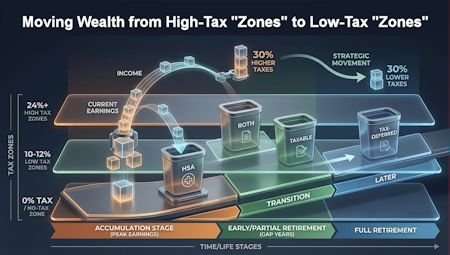

Life Stages

In the FI/FIRE community, the strategies involved generally fall into 3 different stages of the FI journey:

Accumulation: your earlier, high-earning years.

Early/Partial Retirement: low- or no-earning years prior to age 59.5

Full Retirement: low- or no- earning years after age 59.5

We’ll cover tax bracket arbitrage strategies for each of these in the next three blog posts of this series!

We covered U.S. tax brackets and marginal vs effective tax rates in our previous post: Marginal vs Effective Tax Rates. Before we discuss strategies on maximizing our take-home income, (i.e. “tax bracket arbitrage”), we need to know the tools that enable us to do so. Those tools are the different types of investment accounts available to us. These can loosely be grouped into four types (buckets) that you can store your money in.

Those buckets are: Tax-Deferred, Roth, Taxable, and HSA. We’ll cover each below along with one additional for education: 529.

NOTE: As with all FIcology posts, we’re focusing on U.S. taxes and laws. While other countries may have similar concepts, their discussion is beyond the scope of this post.

1) Tax-Deferred – “I’ll Pay Later”

Examples: 401(k), 403(b), Traditional IRA

How it Works: You get a tax break today. Your contributions go in pre-tax, lowering your current taxable income

The Reward: Your contributions grow tax-free UNTIL you pull them out in retirement. These often have some level of employer-matching contributions.

The Catch: You cannot withdraw until age 59.5 or face penalties. Withdrawals are taxable.

FI Context: The most powerful way to reach FI and the number one strategy for earners in the accumulation stage. You avoid paying taxes in a higher tax bracket now, often get matching contributions from your employer, and pay taxes later when you are in a lower tax bracket.

2) Roth – “I’ll Pay Now”

Examples: Roth IRA, Roth 401(k)

How it Works: Your contributions go in post-tax. There is no tax-break today.

The Reward: Your contributions grow tax-free forever. Withdrawals are never taxable. Original contributions can be withdrawn before age 59.5 (although NOT recommended). Employer-sponsored plans may have some employer-matching contributions.

The Catch: While you can withdraw your original contributions at any time (you’ve already paid taxes on those), you cannot withdraw earnings until age 59.5 or face penalties.

FI Context: Tax-free growth and withdrawals forever. You can pull from these accounts without increasing your tax bill—a powerful strategy to prevent hitting higher tax brackets pulling from your tax-deferred accounts.

3) Taxable – “I’ll Pay Now and Later”

Examples: Individual or Joint Brokerage accounts (Vanguard, Fidelity, Schwab, etc.)

How it Works: There are no tax breaks for contributing, and you pay taxes on interest, dividends, and realized (when you sell) gains.

The Reward: Accessible any time. No age 59.5 rules, no penalties, and you benefit from lower Long-Term Capital Gains (LTCG) tax rates.

The Catch: No tax-breaks aside from LTCG (which are significant). You’ll want to favor tax-efficient investments in these accounts.

FI Context: The ultimate flexibility for withdrawal. Having significant funds here can help you retire before age 59.5 (the age you can access your 401(k) without penalties).

4) Health Savings Account (HSA) – “I’ll Never Pay (for Health)”

Examples: HSA (employer-sponsored or through financial institution w/eligible Healthcare.gov plans)

How it Works: You get a tax break today. Your contributions go in pre-tax, lowering your current taxable income.

The Reward: Tax-free contributions and growth. Accessible any time for health care costs.

The Catch: Can only be used for healthcare-related costs. Penalties if withdrawn for non-healthcare costs.

FI Context: This is a literal powerhouse in the FI arsenal. You NEVER pay taxes on this money as long as it’s used for medical-related costs, which we all have. It can even be used for Medicare payments. AND, after age 65, the penalty for non-medical withdrawals disappears. It then acts like a Tax-Deferred account—you just pay income tax on any non-medical withdrawal. This eliminates any concern of overfunding these accounts.

Bonus) 529 – Education Savings

Examples: 529 plans vary by state. Savings plans for higher education expenses.

How it Works: Often states give you a break on state income taxes for contributions. Earnings grow tax free.

The Reward: Tax-free growth. Accessible any time for higher education costs. Powerful savings for your childrens’ college expenses.

The Catch: Can only be used for higher education-related costs. Penalties if withdrawn for anything else.

FI Context: Powerful for funding your childrens’ college education, especially if funded early. May not apply to everyone’s FI planning. Plans and rules vary by state. Included here for completeness.

Pro-Tip: As of 2024, the SECURE 2.0 act allows you to roll over up to $35,000 of unused 529 funds into a Roth IRA for the designated beneficiary (subject to certain rules like the account being 15 years old). This removes some fear of overfunding college savings.

Summary

We covered the four main investment account types that make up the tools for your FI journey. This sets us up to talk about “tax bracket arbitrage” in upcoming blog posts. These different account types enable that arbitrage. Below is a brief comparison of these four account types.

Comparison at a Glance

We also briefly covered a fifth type—529 education savings. If funding childrens’ college expenses is in your future, this should be considered in your FI journey as well.

There are three basic levers we can pull to build wealth: earn more, spend less, and reduce taxes. The first two are easily understood, although not necessarily easy to do. The third, however, is a little more difficult to understand, but still relatively easy to do.

Reducing taxes is one of the best ways to speed up your FI journey and all it takes is learning some relatively simple concepts. These concepts then allow you to employ a number of tax-saving strategies, the most common of which is tax-bracket arbitrage.

For those earlier in their FI journey, tax-bracket arbitrage usually consists of deferring taxes while in a higher tax bracket (your high earning years), until later when you’re in a lower tax bracket (like retirement). For those later in their FI journey, tax bracket arbitrage may mean withdrawing from different accounts or doing Roth conversions to avoid higher tax brackets. For this discussion, we’ll focus on the former.

Before we can understand tax bracket arbitrage, however, we need to understand what tax brackets are, how they work, and what is meant by “marginal” vs “effective” tax rates.

NOTES: Individual state taxes are beyond the scope of this discussion. You will, however, want to factor your state’s income taxes into any tax optimization strategy. FICA taxes are also beyond the scope of this discussion. However, know that FICA taxes are taken out of your pre-tax income and do not change your taxable income.

U.S. Tax Brackets Explained

The U.S. tax system is a graduated system. In simple terms, that means the more income you have, the more taxes you pay. This is done by defining “income brackets”. The concept is simple —for each $ income range (bracket), the IRS defines the tax rate you pay. Below are the federal tax brackets for 2026.

But, before we dive into marginal vs. effective tax rates, let’s cover a couple other terms —”Filing Status” and “Standard Deduction”.

Filing Status

You can file your taxes as 1 of 4 statuses. For most, this will be either Single or Married – filing jointly.

Single: unmarried, no dependents

Married, filing jointly: married and filing together, combining incomes

Married, filing separately: married but filing individual returns

Head of household: unmarried, with one or more dependents (see IRS for full definition)

As you can see from the table above, your income tax brackets vary by filing status. “Married filing jointly” brackets are effectively double “Single” and “Married, filing separately” brackets, for example. That makes sense since two incomes are being filed on one return.

Standard Deduction

The government also allows certain “deductions” that reduce the amount of income you owe taxes on, examples include home mortgage interest and charitable contributions. Rather than require every tax payer to list these deductions, the IRS has defined a “standard deduction” that everyone gets to take. In recent years, this “standard deduction” is so generous that it’s rare to actually itemize individual deductions. For example: In 2022, 91% of tax filers took the standard deduction. The 2026 the standard deductions by filing status are shown below:

You can kind of think of the standard deduction as a 0% tax bracket. For example, Single, and married filing separately, pay no taxes on the first $16,100 of earnings. The difference is, it’s subtracted from your total earnings before to determine your taxable income and then the tax brackets above are applied. An example in the next section will clarify.

Idea: one way to think of the standard deduction is a “0% tax bracket”.

Marginal vs Effective Tax Rates

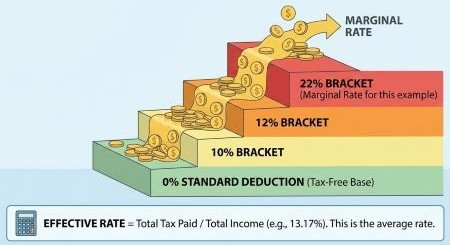

Marginal Tax Rate

Marginal tax rates are simply the tax rates listed on the left side of the “2026 federal tax brackets” table shown above. Let’s clear up a common misconception: many people think whatever tax bracket they fall in is the tax rate they pay on all their taxable income. That’s incorrect. You pay the applicable tax rate for each bracket. The taxable income that falls in each bracket is taxed at that bracket’s rate. That’s the difference between marginal and effective tax rates.

Common Misconception: The tax rate that corresponds with your total taxable income is the tax rate you pay. FALSE —each bracket is taxed at its corresponding rate.

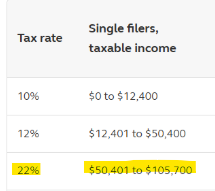

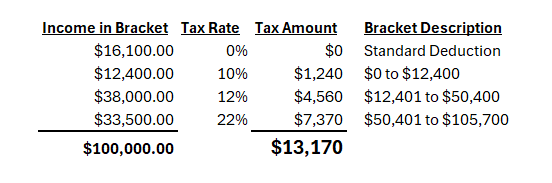

Example: Let’s say a Single filer has $100,000 gross income (that’s total income earned). After taking the standard deduction ($16,100 for single filers), they have $100,000 – $16,100 = $83,900 in taxable income. Using the table above, we see that they are in the 22% tax bracket.

But, that 22% only applies to the amount greater than $50,400. They pay 10% on the first $12,400, 12% on the portion between $12,401 and $50,400, and 22% on the amount over $50,400.

Effective Tax Rate

The above discussion sets us up perfectly to discuss your effective tax rate. The formula for effective tax rate is simply:

Effective Tax Rate = Total Tax / Total Gross Income

NOTE: some people may subtract out the standard deduction and use Taxable Income as the denominator. We’re NOT doing that here because it’s important for the full picture when doing FI tax bracket arbitrage which I’ll cover in a later post.

Total Tax

Back to our single filer earning $100,000 example, to calculate Total Tax we just need to calculate the tax paid in each bracket. We can see that our filer’s total tax burden is $13,170 after breaking her income into the tax brackets as follows:

Total Gross Income

This is simple: $100,000.

Effective Tax Rate = $13,170 / $100,000 = 13.17%

Summary

We’ve learned the difference between marginal and effective tax rates.

Marginal Tax Rate = Tax rate of the highest applicable tax bracket (22% in our example)

Effective Tax Rate = Tax rate calculated across entire earned income (13.17% in our example)

Why is this so important? Because it can make a huge difference doing tax bracket arbitrage for reaching FI. Again, I’ll cover this topic in a later blog post. But as a teaser, consider our single filer example here is determining whether to invest in a pre-tax account (like 401k) or a post-tax account (like Roth 401k). Since our friend’s marginal tax bracket is 22%, she could contribute up to $24,500 ($32,500 if over age 50) pre-tax in 2026. This would defer taxes at the 22% rate. Then at retirement, even if she pulls $100,000 per year from her pre-tax account, she would pay an effective tax rate of 13.17%. That’s 8.83% in tax savings. Plus, she got to earn money on that 22% of taxes the entire time up to retirement!

If I asked you “How long until you get there?”, you’d probably answer me with another question “How until I get WHERE?”. Exactly! You can’t get where you want to go if you don’t first decide where it is you’re going. That’s why having goals is so important. Without a destination in mind, we tend to drift through life. Day-to-day life events lead us around occupying all of our time and energy. These events keep us from making progress on, and even sabotage, our longer-term life needs. Things we know are important, but we haven’t taken the time to define them. Things like: health and wellness, community, retirement savings, and retirement planning.

Life goals like these are not realized in the short-term. They require us to stay on path for much longer periods of time, likely decades. Without explicitly set goals, the day-to-day events will pull us off task. My father once told me:

“If you don’t have a plan, then you’re part of someone else’s plan.“

He’s right. For example: if I don’t have goals for retirement and a plan in place to reach those, it’s going to be REALLY easy for a car salesman to pull me off of that path with a new car and 5-years of interest & payments. It’s going to be REALLY easy for DoorDash to convince me to deliver my meals instead of cooking myself. It’s going to be REALLY easy to drive-thru Starbucks every morning and drop $10 on fancy coffee.

But, if I have defined goals and a plan, a path, I can resist those things. That shiny new car doesn’t look so great when you realize it’ll set your financial independence date back 3+ years. That $10 coffee isn’t so appealing when you realize it maths out to $3,600 / year – money that, if invested, could buy you months of freedom. You get the idea. That is the “Power of the Path”.

Determining Your Destination 🌎

Goals can span any length of time. They can be short-term like “I want to take a vacation this summer”, medium-term like “I want to save for my kids’ college”, or longer-term like “I want to retire at age 59”. The longer the term, the more difficult they are to determine, but, generally, the more important they are. Before we talk about setting goals, let’s talk about life goals – the big destinations in life.

To successfully set long-term life goals, requires some significant self-analysis and reflection. It requires you to answer the questions “What do you want out of life?”, “What matters most to you?”, “What does ‘a life well lived’ look like to you?”. Most people don’t know the answers to those questions. But knowing those answers is critical to setting meaningful goals. There are a number of exercises you can do to help you find those answers; I suggest you try more than one. I’ll list a couple here.

Method 1 – Write Your Eulogy

This is a great way to put your ideal life into perspective. Simply write the eulogy that you’d like given at your funeral. Write down the things you’d like the people attending your funeral to say about you. This is a great way to determine purpose and direction in life. Try writing eulogies from different perspectives, like your: coworkers, adult children, parents, and friends.

There are a plethora of resources online about this exercise. But here are a few questions to ask yourself to help in writing your eulogy:

How did you treat the people in your life?

What principles or knowledge did you pass on?

How did you impact peoples’ lives?

What were your failures and how did you handle them?

What were your important accomplishments in life?

What did you admire? What did you despise?

Take this exercise seriously and spend some time on it. I think you’ll find the results enlightening and clarifying.

Method 2 – Brainstorm Your Wishlist

This is a simple exercise and can be helpful to determine shorter-term goals as well. Spend 20 – 30 minutes writing down everything you want in your lifetime. Don’t filter or limit it in any way. If you want a lake house, write that down. If you want a corvette, write it down. Don’t stop until you have about 100 items spread roughly evenly across the following categories:

Things you want to possess

Things you want to do

Things you want to be or achieve

If you’re like me, you’ll probably start off listing material things. Those are easy. But as the exercise goes on, you’re likely to find that it’s not material things that are really important. As you compile and review this list, the truly important things will begin to be clear.

Setting Your Path: Defining Goals 🥅

If you completed the above exercise, you probably have a number of goals you would like to achieve. Even if you didn’t, you likely already have some things you’d like to achieve. Let’s talk about how to define good goals. For goals to be most effective, they have 3 requirements – they need to be measurable, specific, and have a timeline.

Requirement 1 – Measurable

This is the destination part of your goal path. It states clearly and accurately where you are going – what you are trying to accomplish. Anyone should be able to read your goal and know exactly what it is you’re trying to achieve and determine if you are there or not. Your goal should clearly state “what” and “how much”. For example, “I want to lose weight” is vague and unmeasurable. Instead write “I will lose 25 pounds”. Or instead of “I want to be rich”, write “I will acquire $1 million”.

Requirement 2 – Specific

Both of the examples above bring up a great point – your goals need to be as specific as possible. Making goals specific clarifies what exactly you will be achieving, reducing any ambiguity. It also helps you visualize them along the journey. In our first example, “I will lose 25 pounds”. 25 pounds from what? Am I going to go on a binge gaining 10 more pounds and then lose 25? Make it specific – “I will weigh 175 pounds”.

In our second example, what does “acquire $1 million” mean? Does that include the value of your house, car, possessions? Does it include your emergency or vacation funds? Does it account for any debt? Here’s a better version: “I will acquire $1 million in my 401k retirement account and have $0 debt”. The point is to be able to look at your goal and state definitively that you have achieved it or not. Eliminate any potential gray areas.

Requirement 3 – A Timeline

The second requirement for a goal is simple – when you will complete it by. Goals that don’t have a due date tend to drift indefinitely into “I’ll get to it later”. Let’s continue with our examples from above. We made our weight loss goal measurable by stating “I will weigh 175 pounds”. Lock it in by adding “by when” as follows: “I will weigh 175 pounds by June 1st, 8am”. Our second example could become: “I will acquire $1 million in my 401k retirement account and have $0 in debt by my 59th birthday”.

Staying on Path: Sticking to Goals 🛣️

Once you’ve embarked on your journey (e.g. you’re working towards your goals), you should mostly be on auto-pilot. But at all times, know where you’re at. Be honest with yourself. If you’re lying to yourself about your current location, you’ll never get to where you want to be. Keep your map handy, check that you’re on course, and evaluate your arrival time periodically. This will keep you from veering off path.

Tips for Sticking to Goals

Review your goals daily. There are lots of ways to do this. Print them and tape them on your bathroom mirror. Put a shortcut on your computer home screen. Set a daily timer to remind you. This doesn’t need to take a lot of time, just a quick review each day.

Visualize completing your goals. The more real & vivid your visualization, the harder your mind will work behind-the-scenes to make it happen. If your goal is to own a home, picture in your mind what it looks like: the siding, windows, driveway, front door, layout, etc…

Make some progress every day. Make it a priority to do at least one thing every day that moves you towards each of your goals. Momentum is important on your journey, don’t let yourself coast to a stop.

Carry your most important goal in your wallet or purse. Every time you open your wallet, you’ll be reminded of your goal.

Show up every day even if you don’t do anything. Get to the gym even if you just turn around and leave. Go to your office to write your book, even if you just sit there and do nothing. This keeps your momentum going, builds habit, and reaffirms your identity as someone who “works out”, “writes”, whatever.

Eliminate drag & resistance. Make it as easy as possible to make progress on your goals. Keep workout clothes in your car. Get a gym that’s on your way to work. Make a desktop link to your financial tracking tool on your home screen.

Call to Action 🎬